The shortfall in lithium supply will be met from unconventional sources through technological advances, unleashing economic opportunity, new jobs, and enhancing supply chain security across North America, in our view.

The unfolding energy transition and race to electrify is leaving many rightfully concerned of the looming lithium shortage, including financial groups[1], government[2], and industry.

While the 400% run-up in lithium prices in 2021 was largely driven by long-term demand increases from automaker EV announcements, it has been amplified by near-term supply concerns. Bloomberg notes “a series of near-term risks that threaten deeper shortages”, including plant maintenance, COVID disruptions, and Olympic preparations in China[3].

While the market focuses on ensuring enough lithium is available to meet automaker production targets in the back-half of this decade, an underappreciated long-term threat is growing. According to the IEA, “demand for lithium for use in batteries grows 30-fold to 2030 and is more than 100-times higher in 2050 than in 2020” [4]. Closing a looming supply and demand imbalance will likely come from technological improvements and unlocking lithium found in lower concentrations and unconventional resources.

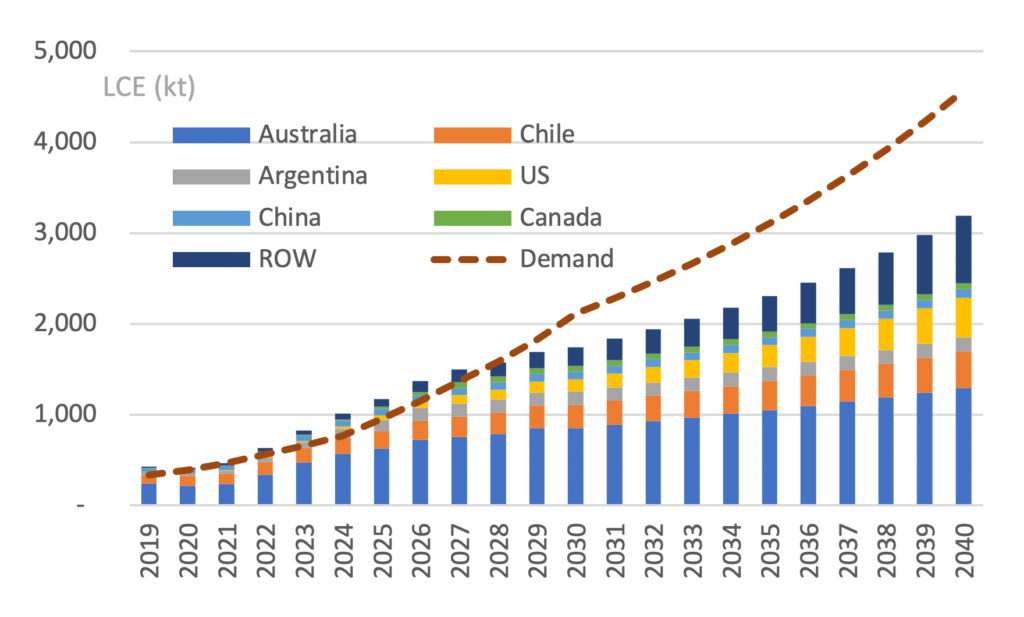

Figure 1: Lithium Supply Outlook by Regions and Global Demand Outlook – 2040E

Source: KMX Technologies, Bloomberg, various investment banks

Today, roughly half of global lithium production comes from hard-rock mining while the other half is from brines that contain lithium. Growing local opposition to hard-rock mining as well as lower costs and carbon intensity[5] from extracting lithium from brine all bode well for additional supply growth from these resources.

As a result, we believe we are at the start of a multi-decade up-cycle in lithium investment that will disproportionately benefit the technologies capable of bringing sustainably mined lithium from brine sources to the market. Luckily, these resources are abundant across North America, with technological improvements poised to position the U.S. as a leading supplier of lithium.

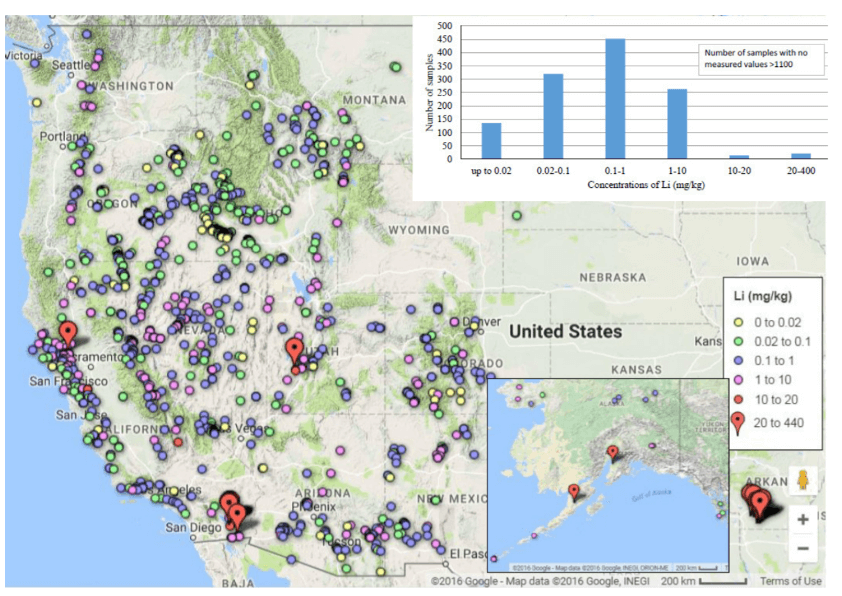

Figure 2: Lithium concentrations in geothermal fluids of the western United States

Source: NREL, U.S. DOE, Neupane and Wendt[6]

Higher lithium concentrations in brine are generally understood to equate to better project economics, all else equal, with most suggesting economic feasibility at a “few hundred parts per million (ppm)”[7]. However, we believe technological improvements will boost project economics and unlock lower concentration lithium resources. Notably, the U.S. DOE’s NREL office cited “potential improvements that could improve economics, in particular improved membrane distillation flux performance”[8].

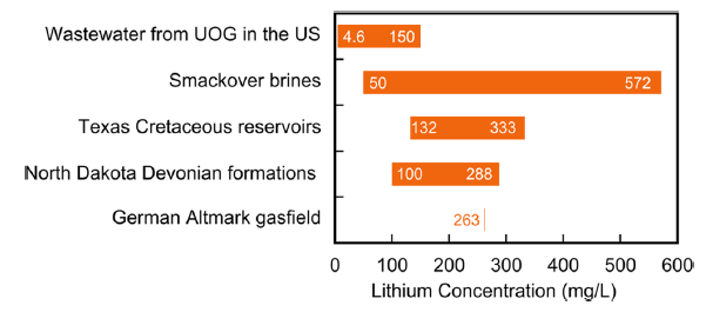

For the U.S., this is a welcome prospect considering the substantial lithium resources available in low concentrations in unconventional sources, such as in produced oilfield water that is a byproduct of oil & gas production, as illustrated in Figure 3.

Figure 3: Li Concentration in water from unconventional Oil & Gas (UOC) in the U.S. and some oilfield brines

Source: Kumar, Fukuda, Hatton, and Leinhard[9]

In addition to unfolding technological improvements driving project economic gains, like membrane distillation (KMX’s underlying technology), we believe the U.S. lithium market will benefit from synergies that arise from a growing crop of smaller unconventional projects, including shared infrastructure, a burgeoning workforce, clearer local regulations, and broader capital market participation.

While much of the attention will likely remain on the marque, large, and high-profile lithium projects globally, an important trend to watch is the rise of smaller decentralized projects with lower lithium concentrations, in our view.

To close the looming lithium supply demand imbalance, look to technological improvements, unconventional resources, and sustainable processes that garner local support. It can be done.

– Zac

Zachary Sadow

CEO

KMX Technologies

- [1] (Wein and Zidle, 2022): https://www.blackstone.com/news/press/byron-wien-and-joe-zidle-announce-the-ten-surprises-of-2022/

- [2] (DOE, 2021): https://www.energy.gov/articles/doe-announces-actions-bolster-domestic-supply-chain-advanced-batteries

- [3] (Lee, 2022): https://www.bloomberg.com/news/articles/2022-01-12/supply-squeeze-risks-are-pushing-lithium-higher-and-higher

- [4] (IEA, 2021): https://iea.blob.core.windows.net/assets/deebef5d-0c34-4539-9d0c-10b13d840027/NetZeroby2050-ARoadmapfortheGlobalEnergySector_CORR.pdf

- [5] (Guthrie, 2020): https://www.miningmagazine.com/sustainability/news/1396497/hard-rock-lithium-faces-esg-threat-roskill

- [6] (Neupane, G., and D.S. Wendt. 2017): “Assessment of Mineral Resources in Geothermal Brines in the US.” 42nd Workshop on Geothermal Reservoir Engineering. Stanford University.

- [7] (Bell, 2020): https://www.thoughtco.com/lithium-production-2340123

- [8] (Warren, 2021): https://www.nrel.gov/docs/fy21osti/79178.pdf

- [9] (Kumar, Fukuda, Hatton, and Leinhard, 2019): Lithium Recovery from Oil and Gas Produced Water: A Need for a Growing Energy Industry | ACS Energy Letters